Data analyzing in emerging market trading

Data analyzing in emerging market trading

Some developing economies are finally seeing light at the end of the tunnel. Global inflation is receding and global interest rates appear to have peaked, prompting a bond-issuance rush by these economies to refinance their debt before the opportunity vanishes. In early January, Mexico, Indonesia, and several other developing economies easily raised more than $50 billion from bond investors.

Yet 28 developing economies—those with the weakest credit ratings— remain stuck in a debt trap with no hope of escape anytime soon. Their average debt-to-GDP ratio was nearly 75 percent at the end of 2023—20 points greater than the typical developing economy. They account for a quarter of all developing economies with credit ratings and 16 percent of the global population. But their collective economic activity constitutes a mere 5 percent of global output, which makes it easy for the rest of the world to ignore their predicament. Their debt crisis, as a result, is silent—and it could intensify.

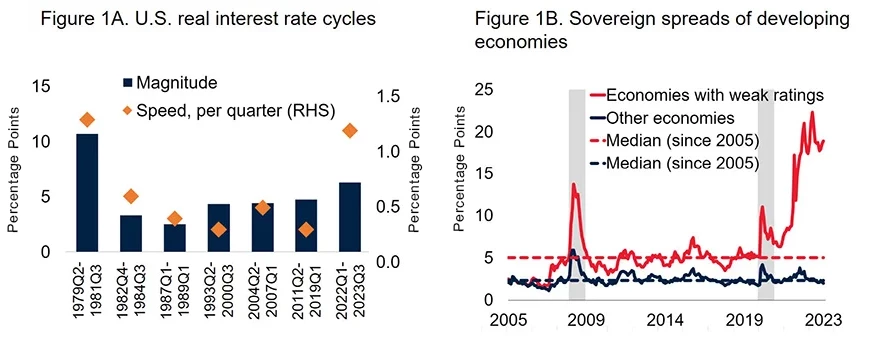

Over the past two years, real U.S. interest rates—a benchmark of the real cost of borrowing globally—increased at the fastest pace in four decades (Figure 1A). Rapid tightening of the U.S. monetary policy has historically spelled financial trouble for many developing economies, as it did in the 1980s. This time, developing economies with good credit ratings have escaped that fate. But the peril has not passed for economies with weak credit ratings. Their cost of borrowing has increased sharply over the past two years: they now face interest rates roughly 20 points above the global benchmark rate and more than nine times that for other developing economies (Figure 1B).

Figure 1. Sharp Increase in the Cost of Borrowing for Developing Economies with Weak Credit Ratings

,

,

Sources: Federal Reserve Bank of St. Louis; Fitch Ratings; J.P. Morgan; Moody’s Analytics; S&P Global Ratings; World Bank.

A. “Magnitude” is the trough-to-peak change and “speed” is the average change per quarter during periods of rising real rates. Real rate is the U.S. policy rate minus one-year-ahead expected inflation from consumer surveys.

B. Median spreads for developing economies with weak credit ratings (sovereign credit ratings are Caa1/CCC+ and below) and other developing economies. The country sample varies over time due to data availability, but it includes up to 70 percent of all developing economies with foreign currency long-term sovereign ratings from the major three rating agencies. Shaded areas represent: September 2008–August 2009 and January–December 2020.

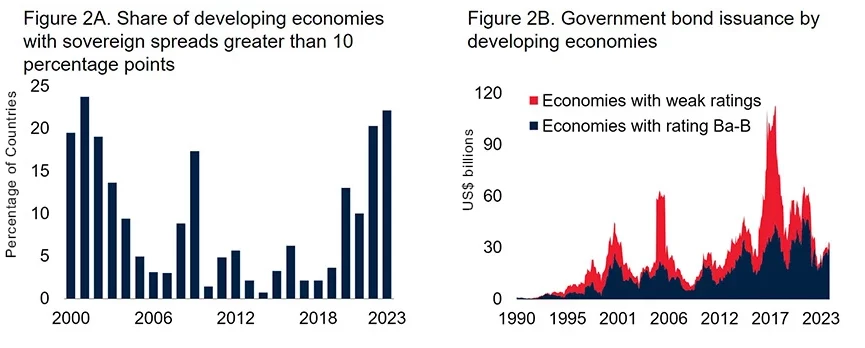

These economies, in short, have now been locked out of global capital markets for more than two years. They have issued almost no international bonds during that time, a barren spell of the kind not seen since the global financial crisis (Figure 2B). Not surprisingly, 11 of them have defaulted since 2020, approaching the total of the previous two decades.

Figure 2. The Longest Dry Spell in Bond Issuance in More Than a Decade

,

,

Sources: Dealogic; Fitch Ratings; J.P. Morgan; Moody’s Analytics; S&P Global Ratings; World Bank.

A. Proportion of developing economies with spreads greater than 10 percentage points, calculated as annual average of monthly values. Of developing economies that had an average spread above 10 percentage points in 2023, one country is rated B3/B- and the rest are rated Caa1/CCC+ or below.

B. Rolling 12-month totals for bond issuance by developing economy governments denominated in major currencies of advanced economies. Last observation is December 2023.

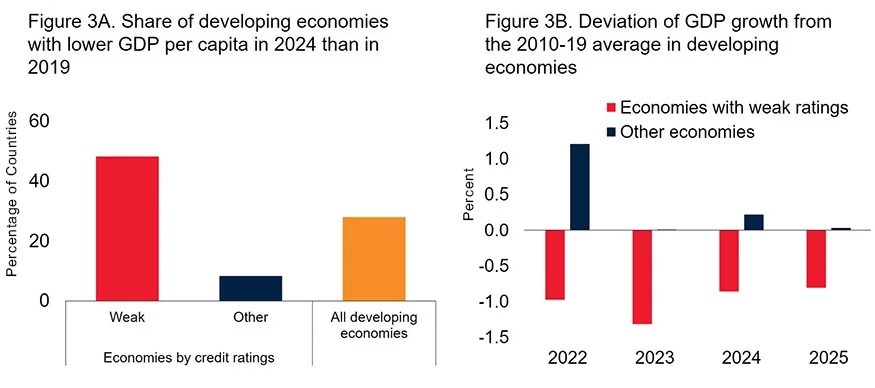

The economic effects have been severe: by the end of 2024, people in nearly half of developing economies with weak credit ratings will be poorer on average than they were in 2019, on the eve of the COVID-19 pandemic (Figure 3A). For developing economies with better credit ratings, the comparable share is just 8 percent. Prospects are unlikely to improve anytime soon: developing economies with weak ratings will grow nearly a full percentage point more slowly over 2024-25 than they did in the decade before the pandemic (Figure 3B).

Figure 3. Slower Recovery and Weaker Growth Prospects

,

,

Sources: Fitch Ratings; Moody’s Analytics; S&P Global Ratings; UN World Population Prospects; World Bank.

Note: GDP aggregates calculated using real U.S. dollar GDP weights at average 2010-19 prices and market exchange rates. Weak ratings defined as Caa1/CCC+ and below.

A. All developing economies includes 99 economies with credit ratings and 46 economies without credit ratings.

B. Median growth rate compared to median of average 2010-19 growth rates. 2023 is an estimate, and 2024-25 are forecasts.

These economies need immediate help from abroad—both in the form of debt relief for some of them and an overall upgrade in the global framework for restructuring debt, which has so far delivered little relief to countries that need it most. But there is also much they can do to help themselves.

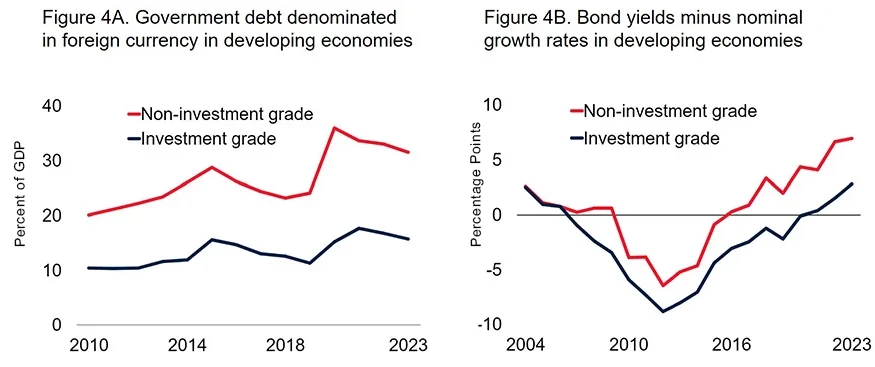

A good start would be to build the fiscal space necessary for economic growth and resilience. Overlapping crises of the past five years deepened the debt challenges, but fiscal imprudence was often the original cause of their troubles. Before they lost access to capital markets, their governments had borrowed too much, especially in foreign currencies—the equivalent of nearly 30 percent of their GDP on average (Figure 4A). That exposed many of them to a familiar vicious cycle: as local currencies weakened, debt costs rose, pushing yields on dollar-denominated bonds as much as 7 percentage points above the growth rates of their economies (Figure 4B).

Figure 4. Larger Foreign-Currency Debt and Higher Borrowing Costs

,

,

Sources: Federal Reserve Bank of St. Louis; J.P. Morgan; Kose et al. (2021; 2022); Moody’s Analytics; World Bank.

A. Median values. Values through 2023Q2.

B. Medians of annual average U.S. dollar bond yields minus trailing 10-year averages of nominal GDP growth in U.S. dollars. Non-investment grade sample is between 15 and 41 economies (of which, between 9 and 19 have weak credit ratings).

Building fiscal space means broadening government revenue bases and prioritizing public spending. Distortive and wasteful subsidies can be jettisoned, for example. On the monetary side, these economies can help themselves by putting in place credible exchange-rate systems and nurturing central-bank independence. These reforms will need to be complemented by improvements in the quality of domestic institutions, so that a more investment-friendly environment can be established. These policy interventions will not be easy to implement. But they are indispensable to restoring economic stability, attracting much-needed investment, and promoting growth.

For developing economies with weak credit ratings, borrowing costs are nine times steeper than they are for better-rated economies

Beyond these 28 developing economies, another 31 mostly low-income countries with no credit rating are already in debt distress or high risk of it. That implies roughly one out of every three developing economies is struggling with high debt in an environment of weak growth, steep borrowing costs, and a multitude of downside risks. An additional shock could easily push more of them over the edge. Should that happen, the silent debt crisis would become an increasingly loud one.

Join the Conversation